Why fragmentation breaks user experience

The current multi-chain landscape functions less like a unified network and more like a fragmented archipelago. Liquidity is scattered across dozens of independent EVM and non-EVM chains, creating deep pools on some networks while leaving others with insufficient depth. This fragmentation forces users to navigate a complex web of bridges, wrapped assets, and disparate interfaces, introducing significant friction that degrades the core utility of decentralized finance.

For the average user, this fragmentation manifests as high cognitive load and operational risk. Managing multiple wallets, monitoring gas prices across different networks, and executing cross-chain swaps are not merely inconveniences; they are barriers to adoption. Each step in this manual process increases the exposure to smart contract vulnerabilities and bridge exploits. The complexity acts as a tax on participation, limiting the addressable market to those willing to endure high technical overhead.

Chain abstraction seeks to eliminate this friction by treating the underlying infrastructure as invisible. Rather than requiring users to understand which chain their assets reside on, the system handles the routing and settlement in the background. This approach mirrors early internet protocols: users do not need to know the physical routing of packets to send an email. By removing the need to think about chains, abstraction promises to restore the simplicity that multi-chain architectures initially compromised.

The economic implications are substantial. Unified liquidity pools can reduce slippage and improve price discovery, benefiting both retail traders and institutional participants. However, achieving this state requires solving the "last mile" problem of intent-based execution without compromising security. The market is currently testing whether these unified liquidity layers can deliver the promised seamless experience while maintaining the robustness required for high-stakes financial transactions.

How Unified Liquidity Replaces Fragmented Pools

Fragmented liquidity has long been the primary friction point in cross-chain interactions. In a traditional multi-chain environment, a user swapping ETH for a stablecoin on a different network must manually bridge assets to an intermediate chain, pay multiple gas fees, and navigate distinct liquidity pools with varying slippage risks. This process is not only time-consuming but also exposes users to smart contract vulnerabilities at each hop. Unified liquidity solves this by decoupling the user's intent from the underlying settlement layer.

The Mechanism: Intent Over Routing

Unified liquidity pools operate on an intent-based model rather than a rigid routing protocol. Instead of specifying a path (e.g., Ethereum -> Bridge -> Polygon -> Swap), the user simply declares what they want to achieve: "Swap 1 ETH for USDC on Arbitrum." The system’s solver network then finds the most efficient path across all available liquidity sources. This might involve settling on Ethereum while delivering assets on Arbitrum, or using a hybrid bridging mechanism that occurs in the background. The user interacts with a single interface, while the complexity of cross-chain settlement is handled by the network’s infrastructure.

Security and Reliability

The shift to unified liquidity introduces new security considerations. Because the system aggregates liquidity from multiple chains, the attack surface expands. However, modern intent-based systems mitigate this through cryptographic proofs and decentralized solver networks. Solvers compete to fulfill intents, ensuring that the best price is offered without requiring the user to trust a single centralized bridge. This competitive landscape reduces the risk of single-point failures, although users must still verify the integrity of the intent execution layer.

Market Context

The volatility of cross-chain activity often correlates with broader market movements. Understanding the underlying asset’s performance is critical when evaluating the efficiency of unified liquidity solutions. The following chart illustrates Ethereum’s price action, which often serves as the primary collateral or settlement asset in these unified systems.

Implementation Checklist

When evaluating unified liquidity solutions, consider the following factors to ensure security and efficiency:

-

Verify solver decentralization and reputation

-

Check fee structures for hidden spread costs

-

Confirm settlement finality times across chains

-

Review smart contract audit history for the intent layer

By replacing fragmented pools with a unified liquidity layer, the user experience approaches that of traditional finance: seamless, fast, and intuitive. The technology handles the complexity, allowing users to focus on their financial goals rather than the mechanics of blockchain interoperability.

Intent-based routing vs manual bridging

Use this section to make the Chain Abstraction decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Key infrastructure layers enabling abstraction

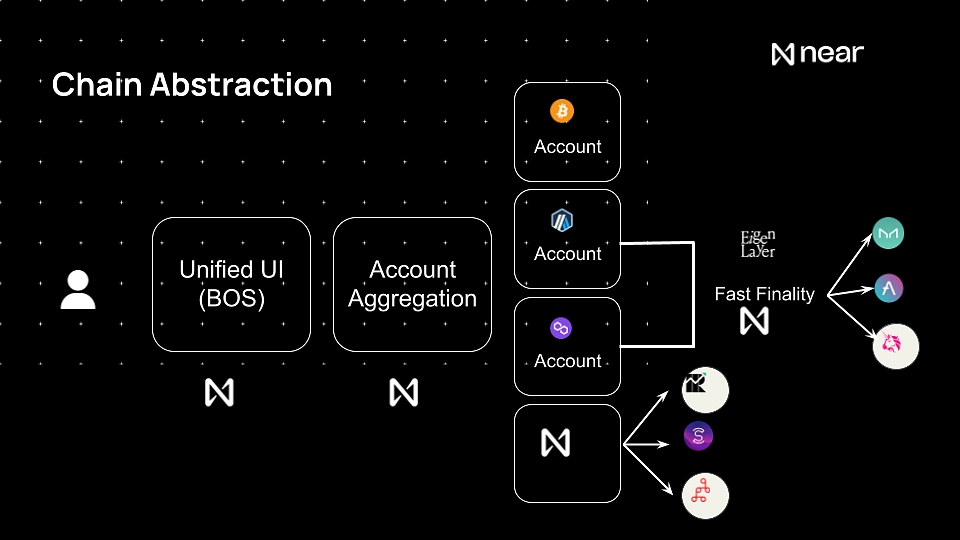

Chain abstraction relies on a specific technical stack to unify liquidity and hide network complexity from the end user. This architecture does not merely wrap transactions; it fundamentally restructures how intent is executed across disparate ledgers. The system depends on three core components: account abstraction for unified identity, cross-chain messaging for secure communication, and liquidity aggregators for capital efficiency.

Account abstraction (ERC-4337) replaces the traditional externally owned account model. By decoupling the key from the address, users can employ social recovery, batch transactions, and sponsor gas fees. This layer ensures that the user’s identity and assets are portable across chains without requiring manual bridge operations. It transforms the wallet from a static key store into a programmable smart contract capable of enforcing complex security policies.

Cross-chain messaging protocols serve as the nervous system of this infrastructure. They verify state transitions between chains, allowing a transaction initiated on one network to trigger an action on another. For liquidity abstraction, these messages carry proof of execution, ensuring that funds moved from Chain A are reliably released on Chain B. Security here is paramount; reliance on optimistic verification or zero-knowledge proofs determines the finality and trustlessness of the cross-chain transfer.

Liquidity aggregators solve the fragmentation problem by pooling capital from multiple sources. Instead of routing assets across bridges, intent-based systems use local liquidity. When a user requests a transaction, the aggregator matches it with a liquidity provider on the destination chain, settling the trade internally while the messaging layer handles the off-chain proof. This approach eliminates bridge slippage and reduces execution time. The infrastructure effectively treats liquidity as a unified pool, regardless of its physical location on the blockchain.

Unified Liquidity and Market Impact

The primary financial promise of chain abstraction is the consolidation of fragmented liquidity into a single, deeper pool. By routing intent-based transactions across multiple chains, protocols effectively aggregate order books that were previously siloed. This aggregation reduces slippage for large trades and improves market depth, particularly for assets that traditionally suffer from thin liquidity on secondary layers.

When liquidity is unified, the marginal cost of capital decreases. Traders and institutions no longer need to bridge assets manually or split orders across disparate exchanges to achieve execution. This efficiency translates directly into tighter spreads and more stable token prices during periods of high volatility. The market becomes less prone to the arbitrage gaps that often exist between isolated chains.

However, this concentration of liquidity introduces new systemic risks. Intent-based systems rely on complex off-chain infrastructure and solvers to match orders. If a major solver fails or a bridge experiences a delay, the entire aggregated liquidity pool can freeze, leading to temporary price dislocations. The reliability of these intent networks is as critical as the depth of the liquidity they provide.

The long-term impact on token valuation remains to be seen. While unified liquidity improves trading efficiency, it may also centralize market power among the few protocols that control the aggregation layer. Investors should monitor solver competition and bridge security audits as key indicators of market health in this emerging landscape.

Account Abstraction vs. Chain Abstraction

Market participants often conflate account abstraction (AA) and chain abstraction, yet they solve distinct structural problems. Account abstraction operates at the user level, replacing the traditional key-based signature model with smart contract wallets. This shift streamlines onboarding, enables gas sponsorship, and groups transactions into batches, but it leaves the underlying liquidity fragmented across separate chains.

Chain abstraction functions as the liquidity layer. It unifies fragmented pools into a single, intent-based interface, allowing users to transact across multiple networks without manual bridging or asset wrapping. While AA improves the digital wallet experience, chain abstraction solves the capital efficiency crisis caused by siloed ecosystems.

For institutional capital, this distinction dictates risk exposure. AA introduces smart contract complexity and potential attack vectors in wallet logic. Chain abstraction introduces cross-chain execution risks, such as bridge failures or intent fulfillment delays. Understanding which layer handles the UX versus the liquidity settlement is essential for assessing security and reliability in 2026.

No comments yet. Be the first to share your thoughts!